A leasing agreement of a pleasure yacht is an agreement between: –

– the ultimate beneficial owner; and

– a Maltese incorporated company

Whereby the lessor (the owner of the craft), which should be a Malta registered company, leases it to the lessee for a consideration. The lessee can be any Maltese or non-Maltese person or company.

The Malta VAT Act stipulates that the lease is a supply of services and the lessor has the right of deduction of input VAT. Any normal lease entered into Malta (excluding the VAT Yacht Leasing Scheme), should have chargeable VAT at the normal rate of 18%.

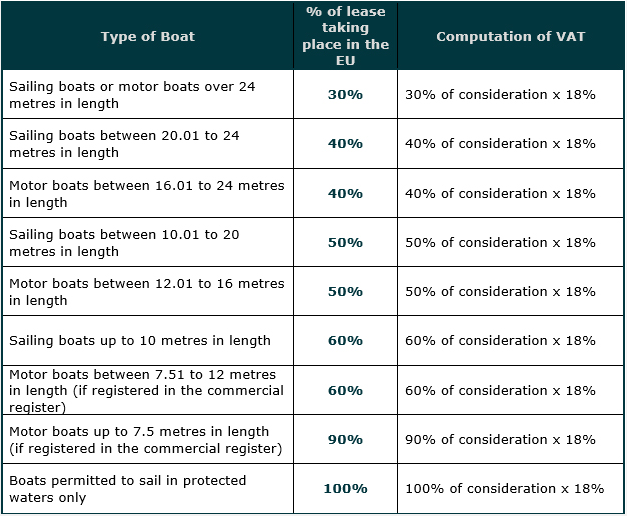

However, when the VAT Yacht Leasing Scheme is applied, the VAT rates charged are reduced significantly based on two determining factors;

– the size of the yacht; and

– the type of yacht (motor vs sail).

The purpose behind the reduction in VAT is to reflect the estimated time in which the yacht would be operated in waters other than the EU territorial waters. Hence, no VAT is charged when the yacht is operated outside of the EU.

Obviously, this is something very difficult to determine. A mechanism was put in place by the Malta VAT department when it issued the below table that determines the percentage proportion of VAT to be charged depending on the length and type of yacht: